By Do-Hyun (Kyle) Hong

On April 12th, the U.S. Department of Labor reported that the Consumer Price Index has risen by 8.5% from the previous year (Cox). This is the fastest annual gain since 1981 when the Fed had to raise the interest rate to nearly 20% under Paul Volcker’s leadership. Furthermore, the Department of Labor reported that the U.S. unemployment rate in March 2022 has reached 3.6%, an all-time low since March 2020 (Mutikani). In some sectors, the unemployment rate has even become lower than in the pre-pandemic times.

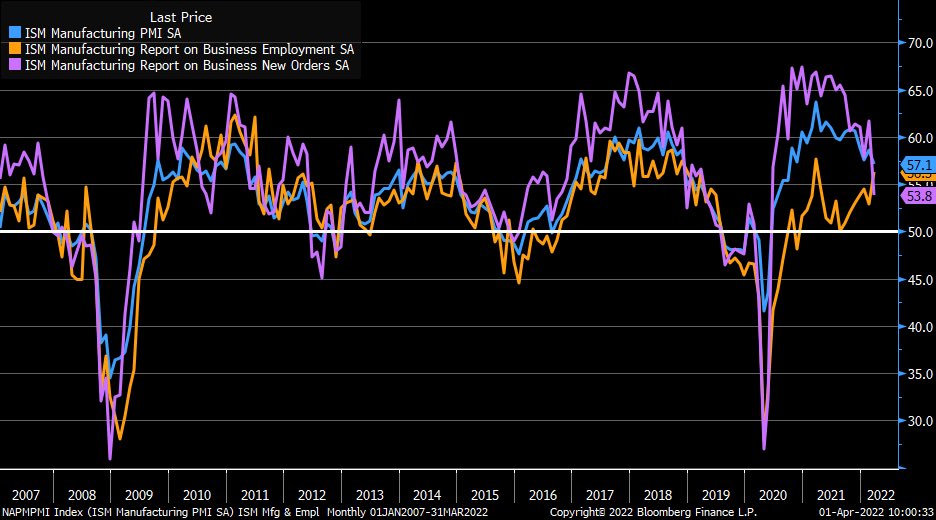

Figure 1 – ISM Manufacturing PMI Index, Provided by Liz Ann Sonders

However, despite these positive economic outcomes, there is a looming fear of stagflation on Wall Street; indexes are starting to show that the U.S. economy has already reached its peak and is starting to experience recessions with inflation rates keep increasing. Above is the trend of the ISM Manufacturing PMI index from the subprime mortgage crisis in the late 2000s to March 2022. A comparison between the trend during the past 2 years and the previous cycles shows that the index has hit its peak in early 2021(Sonders). Since then, it has been consistently going down, resembling the recession stages of previous economic cycles. Furthermore, the U.S. consumer sentiment index, a measure of U.S. consumers’ confidence in personal finances and business conditions, has hit 57.1, the lowest level in the past 5 years (Ycharts). What’s even more alarming is that the index is at a lower level than the April 2020 level of 71.80, when the effect of COVID-19 on the global economy was at its height (Ycharts).

As a response, an increasing number of Fed officials are pushing for interest rate hikes. On March 21st, the Chair of the Federal Reserve Jerome Powell commented that “the labor market is very strong, and inflation is much too high.” He further said that the Fed will take “necessary steps to ensure a return to price stability” (Cox). Given that this comment was already given out when the CPI index was at a lower level, it is now even more likely that Powell will do as he has said. It is important to note that dovish members of the board are also supporting such comments. Dovish is a term referring to Fed board members who prioritize providing liquidity to the market and are hesitant about raising interest rates. On April 14th, John Williams, the president of the Federal Reserve Bank of New York, said on Bloomberg that the “Federal Reserve should reasonably consider raising interest rates by a half percentage point at its next meeting in May” (Dunsmuir). Since Williams has shown dovish behaviors throughout his tenure as a member of the Fed board of directors, this is a signal that even dovish officials in the Fed are starting to think that the ongoing inflation – or potential stagflation – would not be solved with mild interest rate hikes.

Consequently, this has made the stock market more volatile. The S&P 500 index dropped 10% just in January of 2022 from 4700 to 4300, returned to 4500 in early February, dropped back down to 4100 throughout late February and early March, and then sharply increased back to 4600 in the second half of the month. As of April 25th, the index is back down to 4296.12. These fluctuations reflect the uncertainty that investors are feeling in the financial market this year. What’s adding more to the uncertainty is that the midterm election is scheduled in November; this implies that the volatility that the stock market is experiencing may not end even at the end of the year.

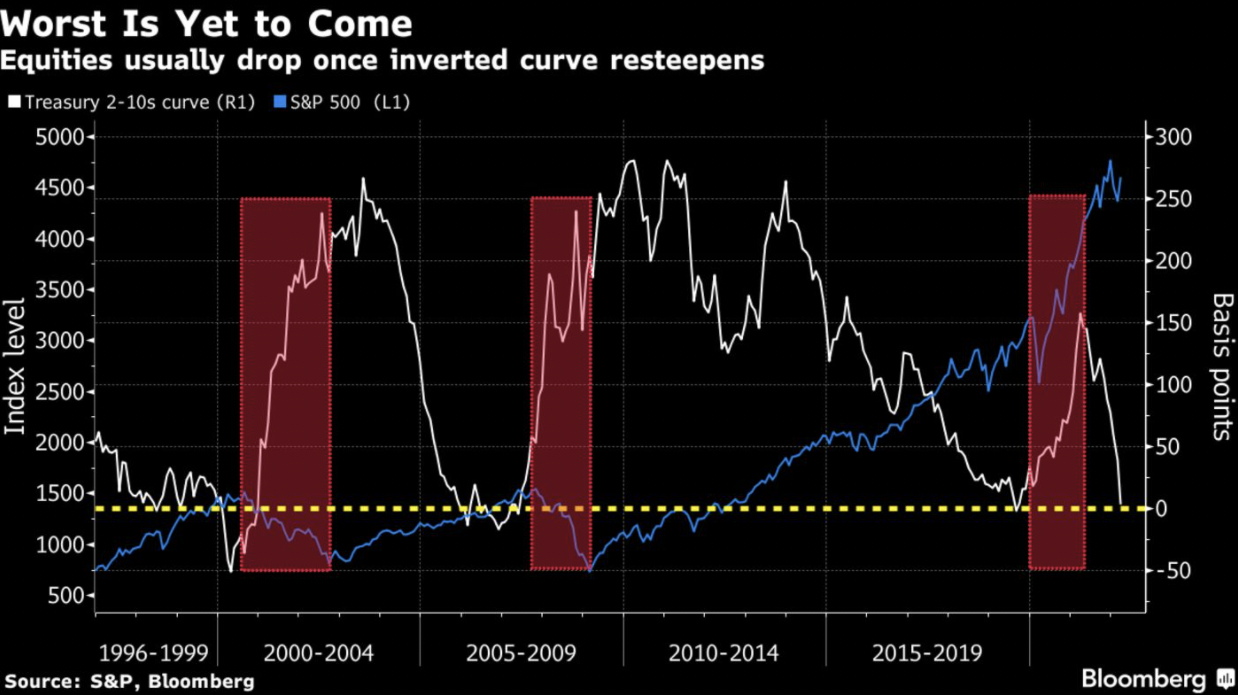

Figure 2 – S&P 500 and Treasury 2-10s Curve, Provided by Alex Millson of Bloomberg

The uncertainty has also been reflected in the bond market as well. On April 1st, 2022, for the first time since 2019, an inverted yield curve happened (Millson). This means that the bond yield rate for the 2-year U.S. Treasury bonds surpassed that of the 10-year U.S. Treasury bonds. This means that the investors are evaluating that short-term uncertainties in the economy are greater than potential long-term risks. At a first look, this may not mean much. However, the problem is that equities usually drop once the inverted curve returns back. Above is the chart comparing the S&P 500 index and the Treasury 2-10s curve which shows the difference between the 10-year bond yield rate and the 2-year bond yield rate (Millson). The areas colored in red are clearly showing that the S&P 500 index tended to decline once the difference between the yield rates started to return back to normal.

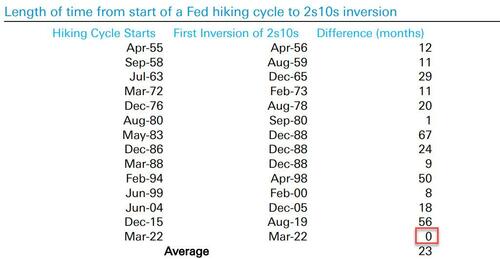

Figure 3 – Length of time from the start of a Fed hiking cycle to 2s10s inversion, Provided by Tyler Durden of NXTmine

Though some say this shouldn’t be a cause of concern as the stock market has generally kept a bullish pattern for 18~24 months after yield curve inversions. This time, however, the yield curve inversion happened at an unprecedented rate. The picture above shows how long it took for yield curve inversion to happen after the Fed started raising the interest rate in history. Unlike the previous cycles that have taken an average of 23 months for this to occur, this time it just took two weeks (Durden). Furthermore, it would be remiss to not mention that the indexes, like the aforementioned ISM Manufacturing PMI index, are showing that the recession might have already started. It seems that we can’t really be at ease with what’s gonna happen based on past experience this time. We have to be prepared for the possibility of a bear market starting much faster than before.

Investors are watching the global economy with bated breath as the financial market is passing through a period of uncertainty. However, one thing seems clear: this cycle is happening at a rate only comparable to the stagflation in 1980 and no one knows how long it will take for this cycle to end. Yet, tumultuous times like now are when we need to remind ourselves of a mantra that has been on Wall Street for decades: Do not fight the Fed. Investors will need to align themselves with the Fed and come up with portfolios that will defend their assets in the coming era of inflation and recession.