Written by Tarini Sathe

The global Coronavirus outbreak highlighted many problems with various systems and institutions on different scales; one of the biggest problems it exposed was the weakness of supply chains across global industries. A supply chain is a network of entities or stakeholders involved in the production process of a good; the chain begins with the producers of raw materials and only ends upon delivery to the consumer. Optimizing supply chains ensures greater efficiency at lower costs, which is crucial for firms to stay competitive (Hayes, 2023). The shutdown of the world disrupted the flow of production at every level—creating massive supply shocks—with recovery still ongoing. However, it has also provided opportunities for firms to rebuild and strengthen their supply chains. Therefore, it is important to look at how the pandemic affected supply chains globally, the weaknesses it exposed and how they are recovering three years post-Covid.

When countries went into lockdown, only essential industries (pharmaceutical, etc.) remained functional while the majority of other industries temporarily shut. This disrupted and slowed the rate of production at all levels of the supply chain (Yadav, 2023). Manufacturing industries with in-person labor dealt with illnesses, Covid distancing and testing protocols, and lack of public transport—all of which caused worker shortages, resulted in less productivity, and a reduced ability to complete orders on time. Moreover, closed airspaces and ports hampered shipping efficiency (Yadav, 2023), and with longer routes or alternate transportation being used, delivery time and costs went up—further delaying the production and delivery of the finished goods.

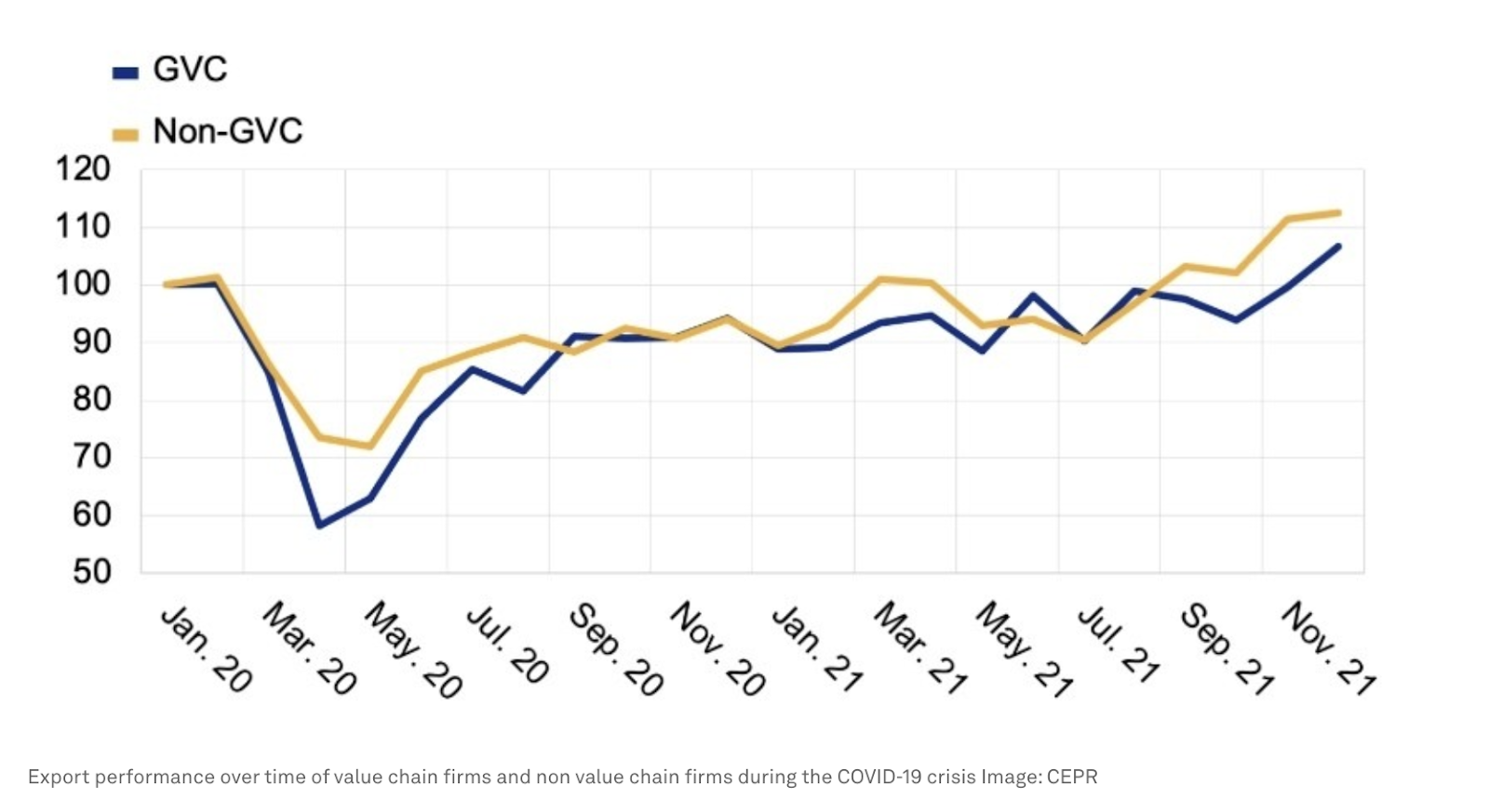

Some of the most affected entities were firms part of global value chains (GVCs)—ones that both import material and export their manufactured product. GVC firms were affected by shipping and international trade issues more so than firms that simply imported or exported (Lebastard et al., 2023). In addition to actual production hurdles, they faced shortages and higher costs to import required (raw) materials, as well as weaker foreign demand for their product and shipping challenges. Lebastard et al. (2023) did a study—with results analyzed on the World Economic Forum— on all the French firms trading internationally to understand the links between supply chains and exporting activity during the pandemic, and further looked at the trends of GVC firms versus non-GVC firms. In order to better understand supply chain and export patterns with context to Covid developments, they looked at three time periods: February to April 2020, the beginning of lockdowns and abrupt production halts; May to August 2020, which was a period of some recovery; and September 2020 to the end of 2021, when supply chain disruptions intensified (Lebastard et al., 2023). Their findings show that “participation in GVCs increased firm vulnerability to the pandemic,” (Lebastard et al., 2023); GVC firms were at greater risk of facing losses, had little cash flow and much-delayed production and delivery timelines. Being doubly affected by international supply shocks, which resulted in this vicious cycle of delays, ensured that it took much longer for GVC firms to get back on track with production. While there was some recovery in the second period, the third period and intensification of Covid and disruptions had a “relatively greater impact” on the exports of GVC firms (Lebastard et al., 2023). In fact, it took until after December 2021 for GVC firms to regain their January 2020 nominal export levels, whereas non-GVC firms had a much quicker recovery—nominal exports reached January 2020 levels by March 2021, and exceeded pre-pandemic export levels by September 2021 (Lebastard et al., 2023). The graph below depicts the same; for all exporting firms in France that have been categorized as GVC or non-GVC firms, their export performance over the time periods in the study has been graphed.

Another issue that the study touches upon is how affected a firm was by supply chain disruption depending on how downstream or upstream the GVC firm was in the supply chain—downstream being tiers that involve the movement of the finished product. It found that downstream GVC firms were more heavily affected than upstream ones (Lebastard et al., 2023), and therefore continued the cycle of creating more (intense) supply shocks. This goes hand-in-hand with a supply chain weakness exposed to firms during this time—not fully understanding every tier of their supply chain and therefore not foreseeing their own production challenges. While firms analyze their sourcing statistics, not many look beyond the first tier to ensure that sources are diversified. However, it is the second and third tiers of the chain coming from regions that firms have actually moved away from—for good reason—that disruptions are rooted in (LaRocco, 2023). Tiers two, three, and lower tend to be located in economically weaker regions—for cost benefits, access to specific resources, etc.—which were majorly affected by Covid and struggled to rebound, thus affecting the production capabilities of firms with otherwise stronger sources of supply. As a result, firms have had to reevaluate their production flows and partnerships—identifying inefficiencies and unnecessary complexities and prioritizing collaboration and transparency with the end goal of a streamlined production process from start to finish (Vitasek, 2023). The silver lining, though, is that these reevaluations have and will continue to enable firms to better optimize cost and efficiency, thus providing consumers with better goods, all the while having facilitated a smooth supply chain experience.

Not only have firms had to reevaluate the complexities of their supply chains, the pandemic has also shown them how putting (almost) all your eggs in one basket leaves you with very few options in times of crisis. Firms had relied massively on China for manufacturing and during the pandemic, with China’s ‘Zero Covid’ policy and shutdowns, supply logistics, deliveries, etc. got knocked out of whack—leaving them in the lurch. Zac Rogers, an assistant professor of operations and supply chain management at Colorado State University, said, “In 2019, we had basically all of our chips in on one hand… things are built in East Asia, come… through the ports in Southern California, they get… distribute[d] to the East Coast,” (Wallace, 2023). He also said that “companies are embracing different paths for the supply chain, whether it be in Vietnam, Bangladesh, Central America, or domestically,” (Wallace, 2023) because even though they cannot cut off China completely, the need of the hour is to diversify production sources in order to be more resilient. The Lebastard et al. study also indicated that diversified supply networks (looking at core imported inputs) of firms served to buffer the impact of supply shocks more so than firms without such networks. Additionally, firms diversifying their supply chains means that they are no longer as vulnerable, and potential future shocks can be better absorbed—particularly ones that are China-centric. In Rogers’ words, Covid was a “trigger” to exposing the state of global supply chains (Wallace, 2023), and this has been an opportunity to strengthen them and make them more resilient to future shocks.

Over the last three years, supply chain activity has begun to recover, although there are still ongoing disruptions at various tiers of their production processes. The pandemic has ensured that firms look inward and evaluate their practices in order to become more efficient and resilient. In fact, a McKinsey report states that “future supply chains will need to be much more dynamic—and be able to predict, prepare, and respond to rapidly evolving demand and a continually changing product…” (Vitasek, 2023). Ultimately, despite the devastation of the pandemic and the havoc it wreaked on global production and supply chains, firms and industries must use it as an opportunity to become more resilient and revolutionize their partnerships to suit the dynamic nature of current consumer demand.

Works Cited

Hayes, A. (2023). The Supply Chain: From Raw Materials to Order Fulfillment. Investopedia. https://www.investopedia.com/terms/s/supplychain.asp#toc-what-is-a-supply-chain

LaRocco, L. A. (2023, January 27). Another Covid Surge in China Is the Global Supply Chain’s Biggest Fear, but It May Be Overstated. CNBC. https://www.cnbc.com/2023/01/27/another-covid-surge-in-china-is-the-global-supply-chains-biggest-fear.html

Lebastard, L., Matani, M., & Serafini, R. (2023, March 30). Understanding the impact of COVID-19 supply disruptions on exporters in global value chains. World Economic Forum. https://www.weforum.org/agenda/2023/03/understanding-the-impact-of-covid-19-supply-disruptions-on-exporters-in-global-value-chains/

Vitasek, K. (2023, June 15). How Strategic Partnerships Simplify Post-Pandemic Supply Chains. Forbes. https://www.forbes.com/sites/katevitasek/2023/06/15/how-strategic-partnerships-simplify-post-pandemic-supply-chains/?sh=624c643a2a24

Wallace, A. (2023, January 16). Covid broke supply chains. Now on the mend, can they withstand another shock? CNN Business. https://www.cnn.com/2023/01/16/economy/supply-chain-outlook-2023/index.html

Yadav, S. (2023, July 11). Supply Chain Management in a Post-Covid World. Forbes. https://www.forbes.com/sites/forbesbusinesscouncil/2023/07/11/supply-chain-management-in-a-post-covid-world/?sh=792c987c5462