Written by Oscar Soberg

The Economics of Supertall Buildings

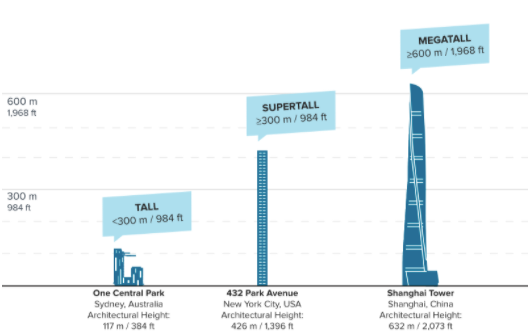

Since the first skyscraper was erected in Chicago in 1884, it seems buildings have only gotten taller and more complex. These modern feats of engineering and design appear to defy nature as they soar up into the sky, and well beyond the clouds. Professionally named “supertall buildings”, these structures reach anywhere from 300 to 600 meters in total height, and number over 170 across the globe with many more under construction (Routley, 2020). Geographically, over half of all supertalls are located in China, with around 17% in the UAE, 9% in the US, and the rest scattered around the world (Routley, 2020). Most of these buildings serve at least one of two important functions: they offer apartments for rent, or office space for lease. Many will also incorporate commercial retail, or even leisure activities. With such details in mind, we can only wonder how these fascinating structures are built and how they are designed. Let’s look deeper into the conditions and underlying risks that come with supertalls, and how they can possibly make economical sense.

The financial view of supertalls can be easily split into the classic categories of risk and reward, of costs and benefits. These buildings generate revenue in a variety of ways, but there are a number of factors consistent across all supertalls.

By far the most crucial aspect, in the eyes of the investor, is ensuring the building will be occupied. As a vacant supertall will never turn a profit, securing leases for these buildings can often be the dealmaker—or breaker. Typically in the US, developers are required to lease up to 50% of the building in advance of construction in order to secure enough backing from investors to support the project (T. Soberg, personal communication, October, 23, 2021). While these leases reduce risk for those building and financing the supertall, they can increase risk for those planning on occupying it. As supertalls take time to build, another issue to be touched upon later, leases must be signed years in advance. These potential tenants rely on the building being completed on time in order for them to have a place to live or work in the coming years. As such, a critical point must be reached where investors not only feel confident enough to push the project forward, but to see it through to completion.

Both developers and investors are drawn to supertalls over comparably smaller skyscrapers for a simple yet relevant reason: they are ridiculously tall. Supertalls are a way for these firms and individuals to put a lasting stamp on the skyline of a major city. They tower over their surroundings and become instantly recognizable structures. There is a very real value that comes from owning such coveted real estate. However, even still the simple title of status and prestige is not single-handedly going to pay back the millions of dollars invested into the project.

What status does provide, though, is an increase in value to neighboring properties. Oftentimes developers own not only the area on which the building resides, but also that which surrounds it (Apipattanavis, n.d.). This means that by building and financing a supertall, they can potentially earn additional profit from the increase in local property value. In addition, a supertall will likely bring more economic activity to the surrounding area, only increasing the return on investment—appealing to developers and investors alike.

Regarding the costs of building a supertall, a few key factors include construction time, efficiency, and material costs. Oftentimes supertalls can have completion dates more than a decade in the future, meaning there is a dramatically increased risk of volatility in the market. If, for example, concrete was chosen for much of the structure, but a recession hits five years later and concrete prices soar, what adjustments can the developer make, or would the project go down the drain? Not only that, but supertalls must take into account the efficiency of the construction process. A supertall needs to hit a sweet spot in height where the marginal benefit from each additional floor is not less than the cost to build that floor. This “sweet spot” must take into account worker productivity, local labor/material/operational costs, and of course functionality of the finished product.

With so many variables and so much risk surrounding a supertall project, it seems just shy of a miracle that they ever materialize into a finished product. Thankfully, these problems described before are not without solutions, some of which are quite clever. Here is where the truly fascinating question of the economics of supertall buildings can be explored.

One of the more obvious ways for supertalls to speed up construction time and reduce costs is to design the building in an easily replicable manner. Often the term “modular” is applied to this style of construction, where floors are essentially copied and pasted for particular sections of the building. Of course, the whole building is not the exact same, but using this style with taste can allow a building to be functional, profitable, and beautiful all at the same time. One reason these modules help reduce cost is that the workers who actually build the supertall will reach a level of familiarity with their tasks and thus become more efficient (T. Soberg, personal communication, October, 23, 2021).

Imagine there is a section of 20 floors on a supertall where each floor is the same design. The first few floors will take a while to build as the workers are learning exactly how everything comes together. By the 15th floor, though, they have become very familiar with the blueprint and can speed up construction, increasing their productivity. One way architects can make easily-replicable designs is by keeping the core of the building consistent throughout. Typically, the center of the supertall is where the electrical, plumbing, and air shafts, along with elevators, stairs, and much more, are located (Ho, 2007). Keeping the core consistent floor-to-floor speeds up construction time and makes coordination between different construction crews easier.

Additionally, construction time can be reduced by building at different heights at the same time. Again a benefit of the module-style design, workers can build at different “sections” and work their way up, or even towards each other. Owing to the progress of modern engineering and to particular design on behalf of the architects, supertalls no longer have to be built from the bottom up, one floor at a time (Apipattanavis, n.d.). Saving on time is incredibly valuable for supertalls given that it can take a decade for them to reach completion. Reducing construction time minimizes exposure to the fluctuations of the economy, and by reducing risk developers and investors can increase profit.

An interesting question for all supertall projects is what height the building should be. What is the difference between a 100-story building and a 101-story building, and how big is that difference? From the economic perspective, any building should be built with the goal of profit maximization. Essentially, the building should be built until the marginal cost of the next floor is no greater than the marginal benefit. But what factors impact this delicate balance of cost and benefit? Well, the different costs include land, labor, material and operational costs. A simple way of visualizing the per-floor cost is to take the total cost of building the supertall and dividing it by the number of floors. However, in reality the marginal cost is much more tricky. Increases in worker productivity due to familiarity can lower the marginal cost, but taller buildings get exponentially harder to build as they soar into the atmosphere. The marginal benefit, though, is comparably more steady and easier to calculate per-floor. The figure to the right shows an interesting principle of marginal costs per-floor and how they relate to height, which will be explored more closely.

The costs of supertalls are calculated not only for the construction of the supertall, but also for its “lifetime.” A supertall will hopefully remain functional and profitable for many decades, but there will inevitably be a point where it is no longer economically viable. Predicting exactly when this “turn off” point is is extremely difficult and can never be exactly perfect, but 30-40 years is a safe minimum for our purposes. The developer must now compare these lifetime costs with expected lifetime benefits, or income. These lifetime benefits are calculated much the same way as the costs, and involve mostly the income from leases.

Looking around the world, we see very different “sweet spots” for building heights, which begs the question: why? For example, in Chicago the sweet spot is around 55 floors while in New York it is around 32 floors, but in parts of China it can be over 100 floors (Barr, 2019). The 58-story Bank of America Tower in Manhattan, which cost about $37 million per-floor (Barr, 2018) seems foolish compared to the 115-story Ping An International Finance Centre in Shenzhen, China, which cost about $13 million per-floor (Wikipedia, 2021). In fact, if one were to compare all the supertalls in the world by location and cost-per-floor, an interesting trend would show up: taller buildings are not necessarily more or less costly than comparatively smaller buildings (Barr, 2019). Using an artificial “Skyscraper Construction Cost Index” (Barr, 2019) we can directly analyze real-world data to compare the local costs to a base country, in this case the United States. What the chart below shows is that different regions have drastically different cost indexes, and regions such as mainland China and the Middle East—where there are high numbers of supertalls—have some of the lowest cost indexes. The conclusion, then, is that supertalls are not only more frequent in Asia than in North America and Europe, but on average cost less to build per-floor, which can be explained by the large difference in local labor and material costs (Barr, 2018). These local costs, particularly labor, are one of the most dominant factors in determining the height of supertalls and subsequently their economic feasibility.

One way for developers to maximize profit from supertalls, and subsequently mitigate risk, is to make the building mixed-use. Also called multi-program, this type of structure is characterized by the variety of functions it serves—including office, retail, apartment, hotel, and restaurant spaces. Approaching supertalls in this way alleviates much of the risk that a regular single-use building has. Developers and investors essentially use retail space and hotel space to hedge against the possibility of low turnouts for apartment leasing and such. Diversifying the building comes with unique challenges, though, which can be seen in the evolution of the design of mixed-use structures over the past couple decades. What started out as a very rigidly-defined organization has morphed into a design that blends different functions together. For example, restaurants can now be found on upper levels of supertalls, where they evolved from smaller cafes for hotel guests. Lobbies are often no longer on the bottom floor (a space almost strictly reserved for retail) but even so one can find desks and breakout spaces in these traditionally single-purpose areas (Bagley, 2018). All these changes in design enable the building to benefit from the economics of diversity. The downsides are that multi-function supertalls can be more complex financially, and the cost of building higher than single-function supertalls (T. Soberg, personal communication, October, 23, 2021).

Supertalls also bring with their status an increase in foot traffic and economic activity in the surrounding area (Apipattanavis, n.d.). It is undeniable that while the supertall itself may struggle with economic viability, the businesses around it will greatly benefit from the building. In this way, developers can further increase the profitability of the supertall by building it around properties they (or possibly some of their investors) own. The economics of a supertall is not restricted to the building itself, and must consider the adjacent properties. By increasing property value along with local business income, supertalls become very fascinating financial assets.

On the one hand, supertalls are extremely risky and quite costly, while on the other they have the potential to bring in large, diverse streams of revenue. Finding the perfect balance between these two sides is hard work, and there is no clear-cut answer. However, supertalls are proving to be more and more financially viable, particularly in Asia where labor costs are low and projects often receive government backing. The process of building a supertall, from its conception to its realization, is reliant on numerous economic factors and beholden to many fundamental economic principles. Despite these obstacles, supertall buildings continue to be built, continue to amaze, and most importantly, continue to make economic sense.

Apipattanavis, S. (n.d.). Understanding the economics of supertall buildings. Www.aurecongroup.com; Aurecon. Retrieved November 18, 2021, from https://www.aurecongroup.com/thinking/thinking-papers/understanding-the-economics-of-supertall-buildings

Bagley, F. (2018). The Mixed-Use Supertall and the Hybridization of Program. International Journal of High-Rise Buildings, 7(1). https://doi.org/10.21022/IJHRB.2018.7.1.65

Barr, J. (2018, December 17). The Economics of Skyscraper Height (Part I). Building the Skyline. https://buildingtheskyline.org/skyscraper-height-i/

Barr, J. (2019, June 4). The Economics of Skyscraper Height (Part IV): Construction Costs Around the World. Building the Skyline. https://buildingtheskyline.org/skyscraper-height-iv/

Ping An International Finance Centre. (2021, August 30). Wikipedia; Wikipedia. https://en.wikipedia.org/wiki/Ping_An_International_Finance_Centre

Routley, N. (2020, June 13). Charting the Last 20 Years of Supertall Skyscrapers. Visual Capitalist. https://www.visualcapitalist.com/charting-the-last-20-years-of-supertall-skyscrapers/

Ho, P. (2007). Economics Planning of Supertall Buildings in Asia Pacific Cities. In ResearchGate. https://www.researchgate.net/publication/242119246_Economics_Planning_of_Super_Tall_Buildings_in_Asia_Pacific_Cities